State of the markets - Oct 25th

Musings: How I view the current markets and what I am doing about it

This recent positive market action is proving to be quite resilient. It has been tested, time after time in the 3,500s, and yet it keeps bouncing back up.

Chart as of end of day Oct 24th, 2022

It recaptured the 10day moving average on Oct 13th and then took back the 21day moving average about a week ago. The RSI has been trending upwards since end Sept and the MACD is on the upswing (see the chart above).

Earnings

I cannot underscore the criticality of earnings coming out this week.

The few that I am watching...

Tue 10/25 GOOG, ENPH, MSFT, VISA

Wed 10/26 META

Thu 10/27 AAPL, AMZN, INTC, MA, MCD, SHOP

Need I name a group of companies more representative of the US and global economy?

Dividend stocks? Value stocks? Industrials? Tech stocks? You have it all this week.

By the end of this week, 70% of the SP 500 companies will have reported earnings. We will know what we need to know at a macro level about the health of global trade and most industrial sectors.

Additionally, US Q3 GDP report comes out on Thu 10/26.

It is expected to come in at a healthy 2.3%. If it comes in hotter than that, markets will not cheer because the US Fed (FOMC) might see it as a sign that inflation is still sticking around.

Broadly speaking, what we have see so far:

revenues have beat estimates by 1.6% - IBM, KO, SAP, RTX

earnings have beat expecations by 4.5% - GM, IBM, KO, MMM, SHW, RTX, UPS

companies are cutting costs (layoffs, capex, shutting locations etc.) - AMZN, META, MSFT, UPS

brands with pricing power are increasing their rates - AAPL, KO, NFLX, SPOT

supply chain constraints are easing - GM, JBHT, KNX

corporate buyback programs are expanding - JNJ, SNAP, TXN, UPS

foreign exchange headwinds are impacting global businesses - MMM, NFLX

some are still floundering - GE, SNAP

In Q3, I am hyper-focused on these specific metrics and signs of market-leading strength. I want to own companies that are not just surviving.

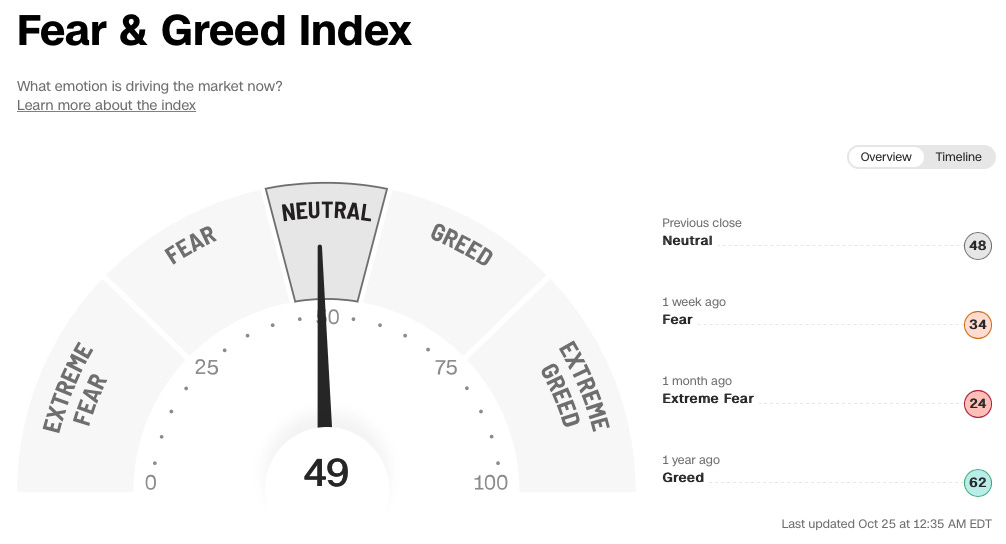

Sentiment

Sentiment has also been turning more positive since Oct 13th.

A month ago, we were at extreme fear levels. A week ago, it improved to "just" fear. And now the needle has swung all the way back to neutral.

China is now broadly viewed as uninvestable, with a more conservative Xi administration taking charge. Look for those investor funds to start flowing to the US....one of the strongest stock markets right now.

Wall street gets less bearish

Multiple analyst notes are giving off hints of less gloom and doom.

Goldman Sachs: "Our recession odds of 35% over the next 12 months are roughly triple the unconditional average for a typical year in recent decades but are well below the 63% consensus odds. One aspect of the consensus forecast that we are particularly skeptical of is the implicit view that rate hikes of the size we expect or just a bit larger will be enough to cause a recession"

Morgan Stanley: "...if global growth weakness continues to weigh on commodity prices, headline PCE inflation may annualized even lower, given tough comparisons to prices last year. So the tanker is turning, we think, and investors should start preparing for pink skies.

...Our core view is that the Fed will not deliver more hikes than priced in, and both inflation and economic data optics will allow them to do so...We think the environment remains conducive to consolidation of Treasury yields, as we head into an FOMC meeting where Powell could reinforce the recent Fedspeak, which seems to be cautioning against infinitely extrapolating higher terminal rates."

Additionally, WSJ reported last week that the FOMC is divided about whether they should continue to aggressively raise interes rates in both Nov and Dec this year. There is a growing expectation that rate hikes will slow down in Dec itself and pause in Q1 2023.

Markets liked these titbits.

Corporate buybacks

Oct 31st will mark the end of the corporate buyback blackout period. 65% of US companies will exit this blackout period next week. $270B+ is waiting on the sidelines in approved share buyback programs. They have 42 trading days left in Nov and Dec to complete these buybacks.

Commodities

Fears of a global economic slowdown have kept commodity prices in check.

China’s demand has slowed down considerably this year.

Wholesale oil prices have stayed relatively modest below $90/barrel since July 1st.

Copper prices have also behaved since mid Aug.

Natural gas prices in Europe tumbled this week due to milder temperatures and major supplies coming in.

The US $ index (DXY) is showing signs of topping.

Risks

There are a few risks that I am concerned about:

Tax loss harvesting - Investors' portfolios have been clobbered in 2022 and many of them are still holding positions that are down 50% or 60% or 70% or more. They are just itching to sell these "loser" positions on any significant rally action. Nov and Dec are peak tax loss harvesting months and this year will be especially busy from that standpoint. This will put downward pressure on stocks and sectors that have been struggling this year - ecommerce, technology and retail.

US election drama - Irrespective of which party wins or loses the election in Nov, there is bound to be a few dramatic events before and after the elections. Markets do not like chaos (just look across the pond to the UK) and any loss of stability could cause stocks to swoon.

Q3 earnings - Any stocks that do not provide guidance (ahem...SNAP...ahem) or are wishy-washy in their forward outlook will be punished. Any companies that are not executing well and at risk of surviving well into 2023, will drop off watchlists and wishlists. Q3 earnings reports are extremely important this year. Investors are tuning in, taking notes and calling out any bullshit.

Volatility - The VIX closed above 27 on Sept 13th and has not looked back since then. Healthy markets usually accompany a declining VIX that dips below and stays below 20. A 20+ Vix usually portends future volatility.

So what's my plan given the state of these markets?

Paid subscribers can read on…

If you are a free subscriber, consider upgrading to a paid subscription to read about my specific portfolio actions and my current holdings. You will also receive my stock picks, buys and sells, actionable market & earnings analysis and other equity and crypto due diligence.