State of the markets - Jan 17th 2023

Markets: What I am watching and doing in the markets this week

In case you missed it, here is a link to the Twitter Spaces investing discussion I had with

and @makeitjain_ . It was a very engaging 2 hour chat on a variety of topics including how markets could perform in 2023, what we should be looking for in upcoming Q4 earnings reports and some of our favorite stocks right now.Markets were closed on Monday Jan 16th, although traders were actively bidding up cryptos over the weekend. More on that below.

Current state

Remember the first-5-day test we discussed last week?

Well, markets rose about 1.4% over the first 5 days of 2023. Looking at data for the last 50 years, 83% of the time, markets closed the year higher when the first 5 trading days of the year were positive. And the average annual return for those positive years was about 14%. So we might have a good year 2023 after all. Fingers crossed!

The SP 500 has risen more than 4% so far this year and word on the street is that markets are getting toppy in the short term and are ripe for a pull back. The RSI indicator above shows the pace of that rise and the need for a pause to digest current prices.

That said, as more stocks rise above their 50 DMAs and even their 200 DMAs, it will bring in more buyers. The stock buyback window ends on Jan 27th and this will further release about $4B of daily corporate purchasing.

So is this a good time to buy or sell or do nothing?

Let me know what you think is the right play here. My opinion is at the bottom of this post.

Sentiment

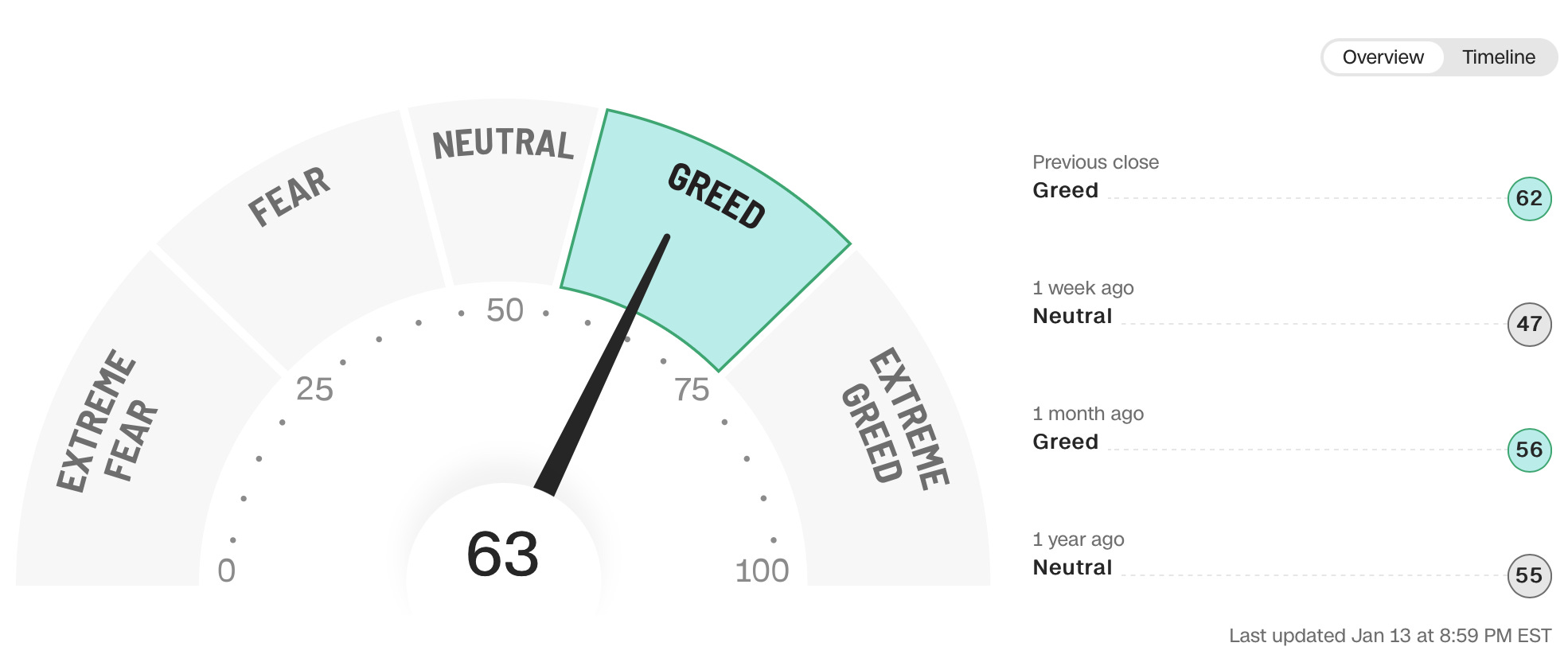

Goldman Sach’s investor sentiment indicator registered one of its most negative signals in the past several months. On the other hand Morgan Stanley’s risk demand indicator is close to an 18-month high, meaning investors are taking on more risk. And the Fear and Greed index continued to consolidate in the Greed area this past week. The contrary signals persist…

Other indicators

US $DXY - keeps dropping and that is generally considered bullish for stocks and crypto.

Oil - showing about a 5% resurgence last week, although it remains in the “good” zone where markets like it. Conoco Phillips is close to sealing a deal with Venezuela to sell that country’s oil to the US. This will increase global supply and put more pressure on oil prices.

Copper - also had about a 5% appreciation last week on hopes of a China re-opening.

Last week

A few key learnings from last week floated to the top of my notes:

Inflation

Dec CPI in the US rose 6.5%yoy, which was a decrease from Nov’s 7.1% and the sixth consecutive monthly drop. It also marked the first month over month (mom) drop of -0.1%mom. The 3-year pre-pandemic average CPI was 2.1%, so we have a long way to go before things get back to normal. Imo, the economy will be looking for that new normal in 2024.

Core CPI, one of the more watched metric by the US Feds, rose 0.3%mom in Dec, following a 0.2%mom increase in Nov. This number ended at 5.7%yoy after logging 6%yoy in Nov.

Dec was marked by lower prices for energy, new and used cars and commodities. Costs for food and shelter remained high as well as for services. Wage growth seems to have slowed a bit and this is what excited markets last week.

Earnings

BAC - beat on revenues and earnings; said that consumer is still strong and credit card usage is higher

C - Q4 income fell by 20% and revenues beat estimates

DAL - Q4 beat on earnings and revenue; Q1 guidance lowered due to higher operating expenses

JPM - beat on revenues; forecasting a mild recession

TSM - record 2022 sales up 42.6%yoy; Q1 guide in line with street estimates, however they warned of a short term dip in demand

UNH - beat on revenues and earnings; reiterated their 2023 outlook

WFC - revenues missed estimates, while Q4 earnings dropped by about 50%. This bank is sicker than it’s peers

Labor

Jobless claims came in at 205,000, lower than estimates and lower than the previous week. Continuing claims also dipped to 1.634M, lower than the previous week. The labor market is still stronger than the US Feds’ targets.

Layoffs continue with:

GS cutting 8% of their workforce (about 3,200 positions).

GOOG cutting 15% of the life sciences unit, a very small cut.

CRM hinting that they will cut more jobs than the 10% announced the previous week.

COIN laying off an additional 20% (950 jobs) in 2023, after an 18% reduction last year.

Crypto.com laying off 20% of their workforce.

Crypto

Binance, one of the few last exchanges standing, has been seeing a flood of outflows and withdrawals, to the tune of about $12B in less than 2 months. According to Forbes, they have lost about 15% of assets since mid Dec.

Meanwhile Bitcoin has risen more than 25% since the start of the year, marked by momentum trading and relatively low volume. The crypto closed above its 200 DMA for the first time in 381 days and traders are expecting it to rise as high at $30k before topping.

Consumers

Univ of Michigan’s consumer sentiment survey rose for the second month to 64.6, although it remains at historical lows. Additionally, consumers have started relying more on credit card debt with about 46% of US credit card holders not paying their monthly balances in full.

Europe

EU inflation appears to have peaked, although it remains high. They are about six months behind the US in terms of their inflation cycle. Central banks are indicating more rate hikes in the future and predicting a more muted recessionary slowdown than previously expected.

Meanwhile EU govts are reducing subsidies (UK govt.’s energy subsidies for businesses) and raising eligibility criteria for social services (France raising retirement age to 64). This might cause some unrest in those countries that typically have stronger labor movements than other continents.

EU Nov industrial production and trade was higher than estimated, largely due to lower energy and commodity prices.

China

Things are still very unclear in China - we do not know the real count of COVID infections and deaths. And it will likely take 1-2 months for economic activity to normalize. Current 2023 GDP estimates are about 5-5.5%, which are healthy by any measure, however lower than China’s historical norms.

Microsoft and OpenAI

MSFT has invested about $10B in OpenAPI, the startup that developed ChatGPT. MSFT continues to aggresively pursue investments in emerging technologies that could bolster their future product pipeline. ChatGPT, while still in it’s beta stage, promises to disrupt search engines and support business use cases in multiple verticals that process large amounts of unstructured data.

Meme-stock trading

The memesters are back as they started heavily speculating on BBBY stock, which is on the verge of bankruptcy.

Key market events

Mon Jan 16th - US markets closed

Tue Jan 17th - Earnings - MS, GS, UAL

Wed Jan 18th - PPI report, retail sales report, Earnings - AA

Thu Jan 19th - Jobless claims report, Earnings - PG, NFLX

Fri Jan 20th - Jan monthly options expiration

The next US FOMC meeting is Jan 31st.

Risks

If markets are on the verge of a short-term top, then this is the week it is likely to happen. Monthly options expirations on Friday Jan 20th will bring additional volatility, especially on Thu 19th.

Beachman’s plan

Here is what I plan to do with my portfolio…

Paid subscribers can read on.

If you are a free subscriber, consider upgrading to a paid subscription to read about my portfolio holdings and actions. You will also receive my stock picks, buys and sells, actionable market & earnings analysis and other equity and crypto due diligence.

Additionally, you willl receive the most important and informative portions of my 2023 repositioning research, analysis and recommendations.