State of the markets - Dec 19th 2022

Markets: What I am watching and doing in the markets this week

First of all, as we get to the final week of the year, I would like to thank all of you for your loyal readership and support over the past 12 months since we launched this publication. It has been a joy for me personally to meet (virtually) and learn from so many of you. I am looking forward to 2023 with optimism and determination. Thank you for your time and your trust.

Now onto the markets…..well, we got the week of consequence that we were expecting.

Nov inflation report came in better than expected

US Feds came out more hawkish than expected

Triple witching options expirations were more volatile than expected

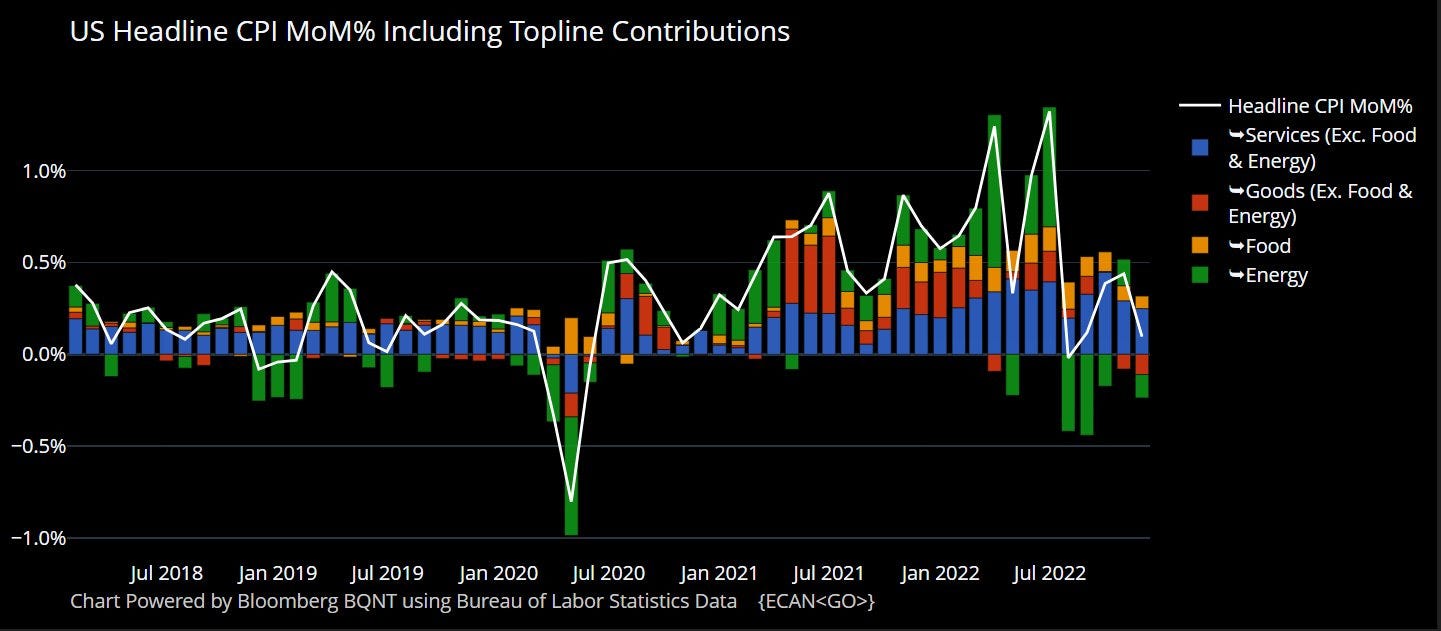

The daily market performance for the week mirrored the CPI graph below…a roller coaster ride up and down.

I continue to advocate using common sense…common investor sense in terms of portfolio positioning leading into 2023.

Here are some things to consider:

Even though Q4 earnings are expected to be lower, much is already priced into stocks based on their Q3 earnings reports and forward guidance. Let’s not forget the deep drops in some stocks right after their Q3 reports were released

Even if markets go down in Q1 or Q2...there will be winners among the drops...stocks & sectors that are recession-resilient

When will the Feds pivot in 2023? They will at least pause rate hikes. Given this expectation, when will markets recover? When will markets price in an economic recovery? Usually about 6-9-12 months in advance

I doubt we are revisiting the lows of mid-Oct. We have tested doing so multiple times already...many of these during one of the worst quarterly earnings season in recent memory....the early Nov timeframe. Count the number of thin candlesticks in the SP 500 and the Nasdaq. They show a battle between the bulls and the bears. No one has won outright since Oct, but the upward trend is clear

I don't think this is the time to get bearish. In fact, it is a time to get a little bullish.

Fears about inflation are easing while fears about an impending recession are increasing. This will color investor sentiment and actions going forward. And we will all be looking for clues in the Q4 earnings reports on how our favorite companies might perform in this new economic-slowdown environment.

And here is another question to ponder:

Can the US Fed steer the economy towards a soft landing?

I will share my thoughts on this matter next week.

BTW, since markets are closed on Mon Dec 26th, the State of the Markets (an abbreviated edition) will be published on Tue Dec 27th.

Current state

After all the shenanigans last week, the SP 500 lost 2.2% for the week. It broke lower than all its moving averages. The RSI and oscillator indicators are trending lower. It is about 10.3% above it’s mid-Oct low that you see on the chart.

Sentiment

The Fear & Greed index finally moved into Fear territory after flirting with Greed levels for a month.

This investor nervousness is also reflected in the higher Put/Call ratios for equities. They are more bullish for bonds this week as markets believe that we are closer to the end of the rate hike cycle. The inverted rate curve is also reflecting this expectation.

Other indicators

US $DXY - Continues it’s downward trend that started in Sept.

Oil - Stays comfortably in the $70s and getting close to it’s lows for the year.

Copper - Is still trying to pick a direction…China reopening is bullish, however global recession is bearish.

Last week

A few key learnings from last week floated to the top of my notes:

Interest rates

The US Feds raised interest rates by 0.50% moving the fed funds rate to a range of 4.25% - 4.50%. Other central banks like the ECB and the BOE also raised interest rates last week by 0.5% each.

Chair Powell and the FOMC dot plot indicated that they expect interest rates to peak in 2023 and to stay above the 5% level because there is still much work left in order to bring inflation under control. Markets did not like hearing this.

Inflation

The US Nov inflation report came in lower than expected.

The Nov reading was 7.1%yoy versus the expected 7.3% and much lower than Oct’s 7.8%. It has decreased for five straight months now, although it is still about three times it’s pre-pandemic levels. Core-CPI for Nov was 6.0%, again lower than the expected 6.1% and Oct’s 6.3%.

The overall rate improved due to falling prices for energy, commodities, cars, medical care and transportation. Food and shelter remain some of the stubbornly high components in the index. US import prices fell 0.6% in Nov and export prices fell by the same rate.

Meanwhile, UK inflation is at 10.7%, Brazil is dealing with 13% inflation and Turkey takes the prize at 85%.

Manufacturing

The US Purchasing Managers Index (PMI) Nov reading dipped to 49% and is signaling a future contraction. The Philadelphia Manufacturing Index rose 6 points but remained negative at -13.8, also signaling contraction. It’s the fourth consecutive negative reading of the index, and the sixth in seven months.

The Eurozone PMI also came in at 49.6%, signaling a contraction on that continent. Germany has slipped to 49.8% from 58.4%. And the UK reading is at 47.3% versus 54.6% in the prior quarter.

Earnings

ADBE - strong earnings report as demand for their software remains steady

BRZE - raised forward top line and bottom line guidance

DAL - raised full year guidance on revenues and earnings, however travel is expected to be slower in 2023

DRDN - beat Q3 expectations and raised forward guidance

ORCL - better than expected earnings report; ERP and cloud segments still strong; Cerner acquisition is paying dividends in the healthcare vertical

X - US Steel reported a better than expected quarter saying that commercial demand for their steel remains healthy. This is interesting and contrary to what I would have expected

Labor

According to the US Labor Department, jobless claims continued to fall to 211,000 for the week ending Dec 10th. Continuing claims were steady at 1,671,000.

Meanwhile, more layoffs were announced with Goldman Sachs giving a Grinchy notice to 8% of their staff effective Jan 2023.

Crypto

Sam Bankman Fried (SBF) was arrested in the Bahamas, pending extradition to the US. Charges from various US regulatory agencies include fraud, wire fraud, conspiracy, securities fraud, securities fraud conspiracy, and money laundering. Speculation is that he will not fight extradition because the US prisons are more comfortable than the one jail on the island.

It was also revealed that US Justice Dept has been investigating Binance. Is it the next major exchange to fall?

And, Brazil was the latest government to announce an official CBDC launch in 2024.

Consumers

The New York Federal Reserve Bank’s Survey of Consumer Expectations reported that consumers are more optimistic about inflation dropping to about 5.2% next year.

However, the near-term focused University of Michigan consumer sentiment index came in with a gloomier 54.7 read, which is near the lowest in about 40 years. Personal savings have come down to $625B, which is well below the $1T level in the past 10 years. Families are feeling the pinch.

Cloud

This was interesting news and I wonder if it is a sign of how hyperscalers will "buy" future business: Microsoft agreed to a 10-year data, analytics and cloud partnership with the London Stock Exchange (LSE). As part of the deal, the company bought a 4% ownership stake in the LSE. What gives?

China

Cases are rising fast as lockdowns and prior restrictions are falling to the wayside. Facilities are checking temperatures and administering rapid COVID tests. Events are getting cancelled. Hospitals and clinics are super busy with the flood of patients.

I read this morning that about 1M deaths are expected in China over the next few months. I am not sure we will ever know the true number of cases and deaths from an administration that massages all their official data.

Chinese retail sales fell 5.9% in Nov, a drastic fall from even Oct and well below economic estimates. Industrial production in the country came in at 2.2% versus the expected 3.6% and less than half of Oct’s 5.0%.

China announced a $143B package to support its domestic semiconductor makers, in the face of US curbs on high-end chip sales.

And the US Public Company Accounting Oversight Board reported that it had secured complete access to inspect China-based audit firms for the first time, resetting a three-year delisting clock for Chinese companies on American stock exchanges.

Key market events

It will be a relatively quiet week and we will gladly take it!

Mon Dec 19 - Homebuilders index

Tue Dec 20 - Housing starts

Wed Dec 21 - Consumer confidence index, existing home sales

Thu Dec 22 - Jobless claims, GDP

Fri Dec 23 - PCE price index, UMich consumer sentiment index

Mon Dec 26 - Markets closed

Risks

I continue to believe that there is now more upside risk in the market after it dropped the indexes lower two weeks in a row. Don’t give up on the Santa rally, just when everyone and their uncle is calling for it’s demise yet again this year

Markets and trading will remain largely muted this week on relatively low volume. Low volume can produce high volatility to the upside or the downside, solely depending on news and events

Beachman’s plan

Here is what I plan to do with my portfolio…

Paid subscribers can read on.