State of the markets - Dec 12th 2022

Markets: What I am watching and doing in the markets this week

So here we find ourselves at the cusp of the final week of any real consequence for 2022.

On Tue, we will get the last retail inflation (CPI) report for the year, tallying price levels for Nov. And on Wed, the US Feds will make their culminating interest rate determination for 2022.

The Dec FOMC meeting is expected to yield another 0.50% rate hike. Most of the committee members have recently indicated, in their public comments, that a 0.50% hike makes sense at this time. Markets are largely expecting this and have priced it in.

Investors will be paying close attention to the previous day’s Nov CPI report as well as the updated FOMC dot-plot from the meeting. The dot-plot indicates where committee members expect rates to end up in 2023. Anything at or lower than the 5% peak expected will be considered bullish. If the dots indicate a higher peak interest rate for next year, markets will likely throw a tantrum. The forecasted 5% peak rate means that rate hikes could continue a bit in Q1 2023, however at a lower pace, followed by a pause and monitor phase.

Current state

The SP 500 index lost about 3.5% last week. It tried, several times towards the latter half, to rally however the bears and tax-loss sellers were firmly in control. With most of the Q3 earnings reporting season behind us, there is little fundamental, company news to drive stock price action. So we dither and flap around in the face of any economic data as well as (and mostly due to) investor and trader sentiment.

Sentiment

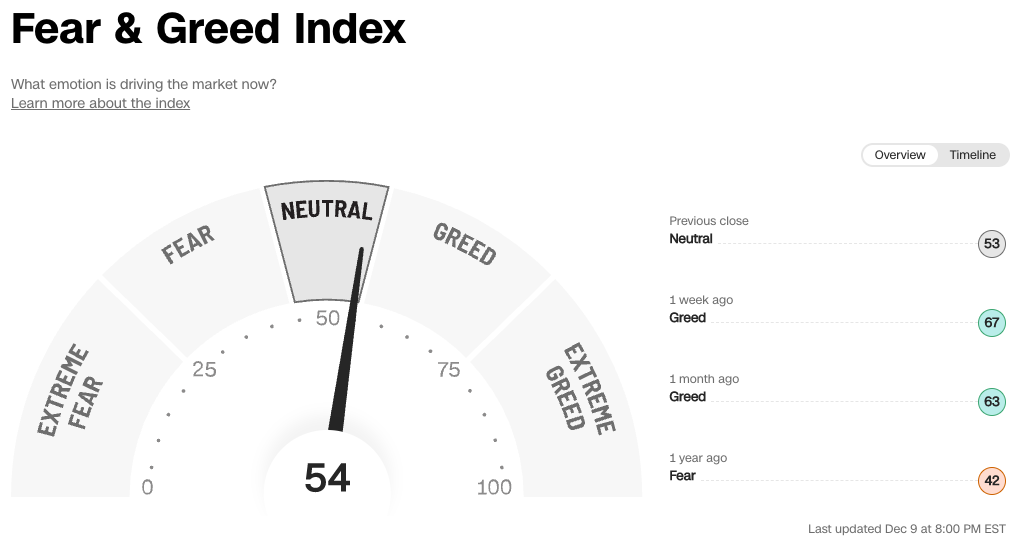

Investor nervousness can be seen in the retraction of the Fear and Greed index from Extreme Greed levels just a week ago to more of a neutral stance. This changed very quickly indeed.

Traders are chasing fewer and fewer opportunities in the face of lower volume. Retail investors are not sure what to do.

And the put to call ratios also ticked several levels higher across the board. More bearish put options being bought for equities and indexes, while bond traders are getting more bullish.

Other indicators

US $DXY - Continued dropping, now in it’s 8th week of declines.

Oil - Oil prices, also, continued to sink to their lowest levels for 2022. By my count, they ended about 11-12% down in one week…yikes! and yay! Several states in the US are seeing gasoline prices of less than $2.90 per gallon.

Natural gas - Europe has cut their demand for natural gas by 25% due to an unseasonably warm winter so far. This took natural gas prices much lower last week.

Last week

A few key learnings from last week that floated to the top of my notes:

Inflation

The US producer price index (PPI), a measure of wholesale inflation, came in at 4.9%yoy, which was a slightly hot increase of 0.3% (economists were expecting a 0.2% increase). The PPI was 7.4% a year ago and it peaked at 11.7% in March 2022. This was the third straight month of 0.3% increases. Excluding food and energy, the Core PPI was up 0.4%, against a 0.2% estimate.

Services inflation accelerated to rise 0.4% for the month, after rising a mere 0.1% the previous month. 1/3rd of the gain came from the financial services industry, where prices increased 11.3%. In contrast, passenger transportation costs fell by 5.6%.

Earnings

AVGO - met revenue expectations, beat earnings estimates and raised forward outlook

COST - fell short of street expectations; recently they had reported depressed sales, especially of big ticket items

DOCU - beat on top line and bottom line estimates

GME - reported a quarterly decline in sales and a wider-than-expected loss

GTLB - beat expectations with a smaller loss and higher revenue and then raised forward guidance

LULU - beat Q3 expectations in sales and earnings, however is forecasting a weaker Q4; inventory levels swelled

MDB - beat expectations and raised forward outlook

Labor

Weekly jobless claims rose last week, however were largely in line with estimates of 230,000. Labor costs rose 2.4%, which was much less than the expected 3.5% increase. Q3 labor productivity rose 0.8%, coming in much higher than the estimated 0.3%.

Meanwhile, layoffs continue in the US with PepsiCo announcing that it would lay off hundreds and Coca-Cola shrinking its workforce via restructuring and voluntary separations. Morgan Stanley is laying off about 1,600 workers (2% of its staff).

Services

The Institute for Supply Management’ non-manufacturing (ISM services) PMI for Nov reported a 57% reading, which was higher than Oct’s 54% read. A number above 50 indicates continued strength and expansion in the services sector, which is running high for 30 consecutive months now. Services based industries make up almost 2/3rd of the US economy. Without these numbers coming down, it will be difficult for the US Fed to achieve it’s 2% inflation rate target.

Real estate

Real estate agencies reported that, across the nation, buyer demand has stalled, home-for-sale supply is slow and prices are sliding. Meanwhile, the 30-year mortgage rate was 6.33% last week as compared to 3.1% a year ago.

Consumers

Dropping consumer sentiment has started showing up in depressed retail sales, especially in the developed world. Retail sales in Europe dropped 1.8% in Oct, the largest drop since July 2021. US auto dealers reported a major slowdown in car sales, the lowest in five years.

China

The Chinese govt. eased several COVID testing requirements and lockdown restrictions. Authorities are now expecting a rise in COVID cases as people try to get back to somewhat of a normal life, including freer movement out and about their cities and towns. Early indications of growing infections can be seen at packed hospitals, clinics and ERs.

China manufacturing for the U.S. is down about 40%, mostly caused by local factory shutdowns and weakening global demand. Their exports fell for the 2nd straight month in Nov - outbound shipments declined 8.7%yoy versus a 0.3%yoy decline in Oct.

Europe

There is increasing optimism in European markets due to lower energy prices and a milder winter so far. The Euro Stoxx 50 index had gained 14% this quarter, close to its best quarterly performance since 2009.

Key market events

Mon 12/12 - Earnings: ORCL, COUP

Tue 12/13 - Nov CPI report, Earnings: BRZE

Wed 12/14 - US FOMC Dec meeting (rate hike expected) & Chair Powell news conference

Thu 12/15 - Jobless claims report, Retail sales report, various US manufacturing index reports, Earnings: ADBE

Fri 12/16 - Triple witching (Expiration of equity options, index options & futures), US manufacturing and services PMI report, Earnings: DRDN

Risks

The Nov CPI report on Tue could surprise to the upside. It could either show a rise in inflation (less likely) or a not-so-strong drop in inflation (more likely). Expectations are for a stronger drop in retail prices. Estimated at a 7.3%yoy rate versus the previous month’s 7.8%

The US Feds could raise interest rates higher than the 0.50% expected. I think this is unlikely and I will be paying more attention to the Chair Powell press conference and the dot-plot data

The biggest source of volatility this week, especially on Wed and Thu will be the options markets’ triple witching expirations in equity options, index options & futures. As traders and investors get closer to the expiration of their options positions, they have to decide whether to close the position or roll it over to the following month. If the events of early-in-the-week are bullish for markets, we could see more buying of call options, further fueling a rise in markets or vice versa.

Beachman’s plan

Here is what I plan to do with my portfolio…

Paid subscribers can read on.

If you are a free subscriber, consider upgrading to a paid subscription to read about my specific portfolio actions and my current holdings. You will also receive my stock picks, buys and sells, actionable market & earnings analysis and other equity and crypto due diligence.