Q1 earnings brief - NVDA

Portfolio: Highlights, trends and comparative performance findings from recent earnings reports

NVDA’s CEO, Jensen Huang, has been talking about AI for years. But most investors were not paying attention to the vision he was painting about the value that AI could bring to our lives and to businesses around us. They continued to focus on the company’s gaming, desktop and crypto mining business. Well, all that changed last week when Nvidia published their Q1 earnings.

Irrespective of whether you are an NVDA bull or bear, you have to respect their report. NVDA told us (and MRVL’s Q1 results confirmed) that most of the existing data centers will have to be re-architected, redesigned and upgraded to truly support generative AI for business usage. NVDA’s H100 GPUs and full stack AI solutions are currently the only products in the market that can provide these capabilities.

Additionally, I would argue that EVEN WITHOUT their big Q2 revenue outlook raise, NVDA has been pivoting towards more positive business performance for 2-3 quarters now. The higher Q2 guidance just cemented the turnaround story.

Let’s take a closer look at NVDA’s Q1 earnings report to understand why…

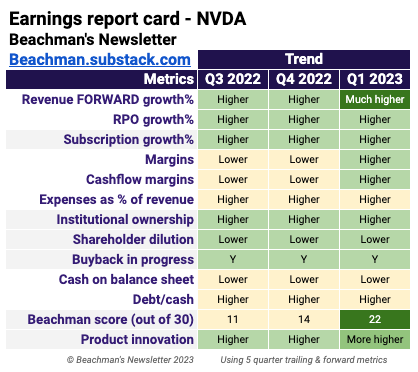

Q1 earnings report card

See detailed financial map at the bottom of this post.

Revenue: Q1 revenue was $7,192M -13% yoy 19% qoq. They beat Q1 consensus estimates by a very healthy 17%.

Gaming revenue was $2,240M -38% yoy 22% qoq reflecting macro driven weaker demand and lower shipments to normalize channel inventory levels.

Data center revenue came in at $4,284M 14% yoy 18% qoq led by growing demand for generative AI and large language models using their NVIDIA Hopper and Ampere architecture GPUs…strong demand from large consumer internet companies, cloud service providers and enterprise customers.

Professional Visualization revenues were $295M -53% yoy 31% qoq due to lower sell-in to partners to help reduce channel inventory levels.

Automotive revenue logged $296M 114% yoy 1% qoq showing strong growth in sales of self-driving platforms and AI cockpit solutions.

Now notice how yoy revenue growth for several segments was better in Q1 versus the previous quarter? And additionally, notice how qoq revenue growth was also more positive in Q1 for these categories? This is a clear sign that NVDA has pivoted to higher growth across most of their product lines.

Forward estimates: Q2 revenue estimate was revised upwards to $11,220M 67% yoy, which includes a doubling of their data center revenue qoq. Full year 2023 estimate was updated to $44,269M 64% yoy. This enormous surprise raise of their forward estimate drove the stock price about 25% higher the next day. NVDA seems to have pulled forward about 2 years worth of data center demand. Remember how cloud stocks did something similar during the COVID pandemic?

NOTE: Analysts are still calculating forward estimates because NVDA’s forward guidance took them by surprise. These unknowns are reflected in the financial map below.

RPO: RPO came in at $639M -2% yoy -2% qoq.

Margins: NVDA’s margins have started expanding again in Q1. Gross margin increased to 65% and is expected to rise further to 69% in Q2. Operating margin came in at $2,140M 30%. EBITDA margin was higher at $2,659M 37%. Net margin expanded to $2,043M 28%. Expenses as a percentage of total revenues have continued to trend lower for two quarters now. Even stock based compensation is well in check at 10% of total revenues.

Cashflows: Cash flow margins also switched to expansion mode in this quarter. Operating cash flow rose to $2,911M 40%. Free cash flow increased to $2,663M 37%. Free cash flow per share rose to $1.07/share.

Cash and debt: NVDA continues to add cash to their balance sheet for the past three quarters. In Q1, they had $15,320M in cash and $11,893M total debt. Their debt to cash ratio ticked lower to 0.78…getting close to my preferred 0.75 range.

Shareholder value: Shareholder dilution continues to decrease with total diluted shares at 2,490M shares -2% yoy. NVDA has spent about $8B in the past year and still has about $7.23B in funds for their share repurchase program. Interestingly they did not buy back any shares in Q1…perhaps they are also waiting for a pullback before repurchasing. They did return $99M to shareholders in cash dividends in Q1.

Institutional ownership increased to 68%. Funds are back in buying mode after taking a break for the past three quarters.

Marketshare: In order to understand why NVDA is considered the leader in the AI space, we have to go back to what CEO Jensen Huang said in this Q1 report.

“The computer industry is going through two simultaneous transitions — accelerated computing and generative AI. A trillion dollars of installed global data center infrastructure will transition from general purpose (CPUs) to accelerated computing (GPUs) as companies race to apply generative AI into every product, service and business process.”

Their data center family of products, includes the H100, Grace CPU, Grace Hopper Superchip, NVLink, Quantum 400 InfiniBand and BlueField-3 DPU. These are all in production and already seeing very high demand from the hyperscalers and enterprise customers. Morgan Stanley put out some research last week estimating that semiconductor chips will be the leading beneficiaries of AI demand for about 1-2 years, followed by demand for data center, networking and storage infrastructure and then lastly higher demand for software AI solutions.

NVDA announced several new data center and AI partnerships with Google Cloud, Amazon Web Services, Microsoft Azure, Oracle Cloud, ServiceNow, Medtronic and Dell.

They added 36 DLSS gaming titles, bringing the total number of games and apps to 300.

They expanded GeForce NOW’s game titles to more than 1,600, including the first Microsoft Xbox game, Gears 5.

They expanded their collaboration with Microsoft to connect Microsoft 365 applications with Omniverse.

NVDA’s automotive design win pipeline has grown to $14B over the next six years, up from $11 billion a year ago, including that EV maker BYD will extend its use of NVIDIA DRIVE Orin™ across new models.

Product: There were, of course, several product updates in Q1 including:

Launched four inference platforms that combine the company’s full-stack inference software with the latest NVIDIA Ada, NVIDIA Hopper™ and NVIDIA Grace Hopper™ processors.

Introduced NVIDIA AI Foundations to help businesses create and operate custom large language models and generative AI models trained with their own proprietary data for domain-specific tasks.

Unveiled the NVIDIA cuLitho software library for computational lithography to accelerate the design and manufacturing of next-gen semiconductors.

Announced it is integrating NVIDIA AI Enterprise software into Microsoft’s Azure Machine Learning to help enterprises accelerate their AI initiatives.

Announced the GeForce RTX™ 4060 family of GPUs, including the advancements of NVIDIA Ada Lovelace architecture and DLSS.

Launched the GeForce RTX 4070 GPU based on the Ada architecture, which enables DLSS 3, real-time ray-tracing and the ability to run most modern games at over 100 frames per second at 1440p resolution.

Announced NVIDIA Omniverse™ Cloud, a fully managed service running in Microsoft Azure, for the development and deployment of industrial metaverse applications.

Announced six new NVIDIA RTX™ GPUs for mobile and desktop workstations based on the Ada architecture.

As a reference, I provided a simple primer on Nvidia’s products in this post.

Valuations: Taking into consideration enterprise value, gross profits and forward growth…..